Short on time? Here's what you need to know

- Underinsurance means your cover doesn’t reflect the true rebuild cost of your property

- If you claim, your insurer may reduce the payout, even for partial losses

- Rebuild costs often change over time, so it’s easy for cover to fall out of date

- High-value homes and specialist features are more likely to be underinsured

- A proper valuation helps make sure everything is covered correctly.

What it means to be properly insured

Most homeowners assume that if their property is insured, they’re protected. In reality, it’s often not that straightforward.

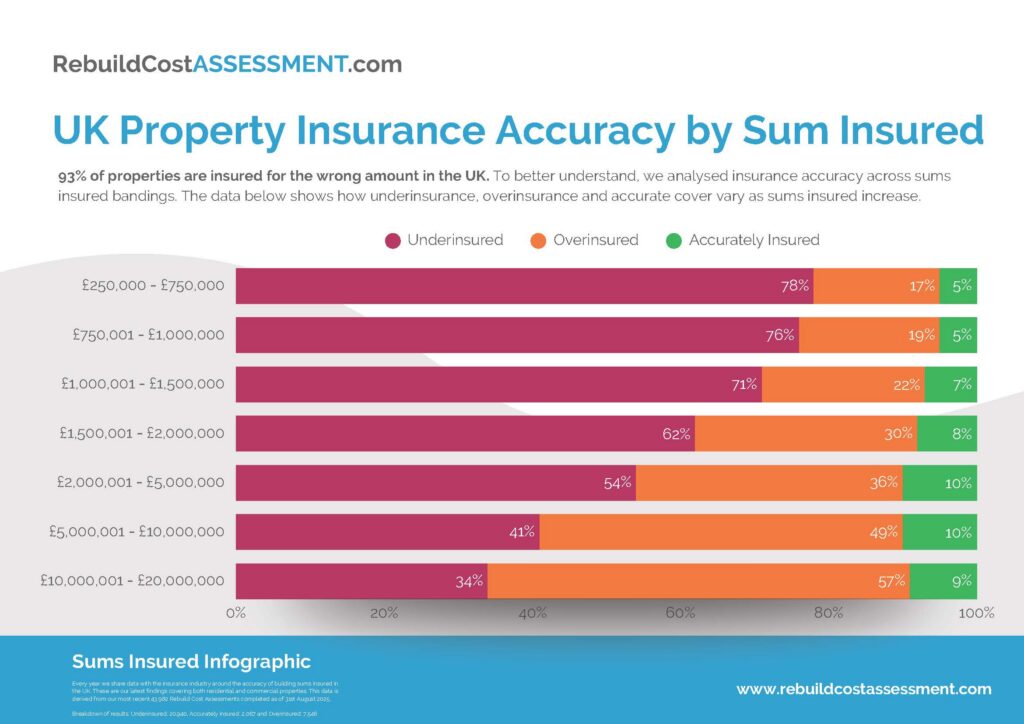

Recent research from Rebuild Cost Assessment found that only 7% of UK properties are insured accurately. The remaining 93% are insured incorrectly, with 70% underinsured and 23% overinsured. In other words, most are not insured in a way that reflects the true cost of rebuilding them.

The same research highlights something many people wouldn’t expect. As property values increase, accuracy doesn’t necessarily improve. Lower-value homes are more likely to be underinsured, while higher-value homes are more likely to be overinsured. Either way, the cover may not reflect the true cost of rebuilding.

This matters because insurance is only really tested when you need to make a claim. If the figures behind your policy aren’t right, that’s when any gap becomes clear.

Underinsurance

It can be tempting to lower your building sum insured to bring premiums down. In practice, that can leave you with a shortfall when you need to claim.

If a property is underinsured, insurers may apply what’s known as the ‘average clause’. This means a claim payment can be reduced in proportion to the level of underinsurance, even if the loss is only partial.

For example, if a property is insured for 80% of its true rebuild cost, a claim could be reduced by 20%. That can come as an unwelcome surprise, especially if you expected the policy to respond in full.

Overinsurance

The same research from RebuildCostAssessment shows that at higher property values, particularly between £5 million and £10 million, overinsurance becomes more common. In some cases, properties are insured for more than their rebuild cost as a way to feel on the safe side, but without a clear basis for the figure.

Johnny Thomson, Head of Strategic Planning at Rebuild Cost Assessment, explains:

‘There’s a common assumption that insurance accuracy improves as property values rise. What our data shows is that this simply isn’t the case. As sums insured increase, behaviour changes, but accuracy does not.’

While overinsurance doesn’t carry the same immediate risk as underinsurance, it can still lead to higher premiums than necessary and a false sense that everything is in order.

What does it mean to be properly insured?

It’s less about insuring for more or less, and more about getting the figure right from the start.

That begins with understanding the true cost of rebuilding your property. This is known as the reinstatement cost, and it’s different from the market value of your home.

A proper reinstatement valuation should take into account:

- the cost of rebuilding the property

- professional fees, such as architects and surveyors

- demolition and site clearance

- the impact of inflation on labour and materials

Without this level of detail, figures can easily be based on estimates or assumptions rather than something more reliable.

Common questions about rebuild cost and underinsurance

What should be included in a rebuild cost?

It goes beyond the structure itself. Professional fees, compliance requirements, demolition costs, and rising construction costs all need to be factored in. These can change over time, which is why it’s important to review them regularly.

What is the ‘average clause’ and how could it affect a claim?

If your property is insured for less than its true rebuild cost, any claim payment may be reduced in proportion to the shortfall.

This applies even if the claim relates to only part of the property. It’s one of the most common areas of misunderstanding, and often only becomes clear when a claim is made.

What if we wouldn’t rebuild in the same way?

Insurance is based on the cost of reinstating what currently exists, not on future plans or intentions.

Even if you choose to rebuild differently, the policy is designed to reflect the current structure and what it would cost to replace it.

Is there a way to avoid getting this wrong?

Accurate valuations make a significant difference. Some insurers offer ‘guaranteed replacement cover’, which can provide additional reassurance, but this still relies on regular review and a clear understanding of the property.

In practice, the most important step is making sure the figures behind your policy are based on a current, reliable valuation rather than an assumption.

Why accuracy matters

The research makes one thing clear. Most people are not getting this right, and it’s not always obvious when a property has been insured inaccurately.

Being properly insured is not about choosing a higher or lower number. It’s about understanding what your property would actually cost to rebuild, and making sure your policy reflects that.

Taking the time to review it properly can help avoid gaps in cover, unnecessary costs, and difficult surprises if you ever need to claim.

If you’re not completely sure your current cover reflects the true rebuild cost of your property, it’s worth reviewing it. A proper valuation can bring clarity and help make sure everything is in place before it’s ever needed. You can contact our team to arrange a review.